TL;DR: Key Takeaways

The Renewal Wave is Now. Millions of UK business energy contracts signed during the 2022-2023 crisis are expiring. If you signed a 3-year deal at the peak, your contract is ending in late 2025 or early 2026.

Rates Have Dropped Significantly. Crisis-era fixed rates of 50-60p/kWh have come down substantially. A typical SME renewing from a crisis-era contract could save £6,000-£9,000+ per year, depending on their original rate and current market conditions.

Prices Are NOT Going Back to “Normal”. Pre-crisis rates of ~15p/kWh are unlikely to return while the UK depends on globally-traded gas. Non-commodity charges - network costs, levies, infrastructure investment - now make up nearly 60% of your bill and are still rising.

Don’t Wait - But Don’t Panic Either. New geopolitical volatility (Iran/Middle East) is causing short-term price swings. Analysts recommend 12-24 month contracts to lock in current rates while staying flexible for projected price drops in 2027-2028.

The Biggest Risk is Doing Nothing. If your contract expires and you don’t act, you default onto deemed rates - typically far more expensive than a competitive fixed deal. Every week of inertia has a measurable cost. Learn how to switch in 20 minutes.

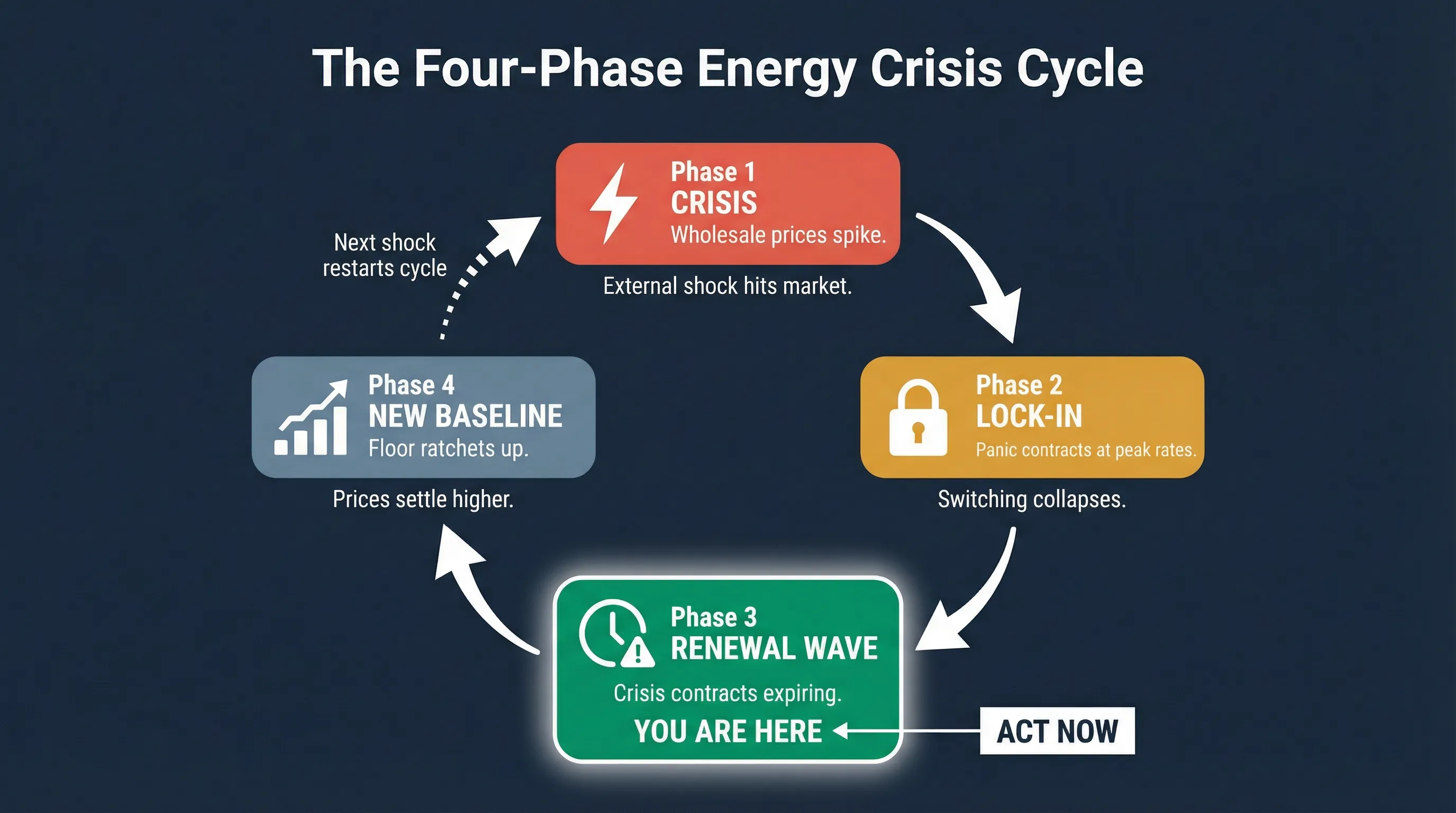

The Four-Phase Energy Crisis Cycle

If you think the 2022 gas crisis was a one-off, it wasn’t. The UK business energy market has a pattern of responding to external shocks in predictable ways - and understanding that pattern is one of the most useful things you can learn about business energy, because it tells you where we are now and what to do about it.

The cycle has four phases:

- Crisis - An external shock (geopolitical conflict, supply disruption, extreme weather) causes wholesale energy prices to spike violently.

- Lock-in - Businesses panic-sign contracts at peak prices, or freeze entirely and fall onto expensive default tariffs.

- Renewal wave - 12-36 months later, those crisis-era contracts expire. Businesses face a critical decision point.

- New baseline - Prices settle, but to date have never returned to pre-crisis levels. The floor has ratcheted up after each major shock due to rising infrastructure and policy costs.

We are currently in Phase 3. The crisis-era contracts are expiring, and businesses that act now can significantly reduce their energy costs. Businesses that don’t act will bleed money on deemed rates until they do.

Echoes of this cycle are visible after previous UK energy shocks - the 2011 Fukushima disaster and Arab Spring (UK gas prices doubled from ~30p to 60p/therm), the 2018 “Beast from the East” cold snap (out-of-contract gas rates spiked by 180%). Each time, a supply shock triggered elevated pricing, followed by a painful renewal period. But the 2022-2023 crisis was unprecedented in its severity for the non-domestic market - SME rates of 50-60p/kWh had never been seen before - and the renewal wave it created is likely the largest in recent memory.

What Happened in 2022-2023 (And Why It Matters Now)

The numbers are stark. In 2021, the UK energy market recorded approximately 4.99 million electricity switches across domestic and non-domestic customers - a healthy, functioning market. In 2022, as wholesale prices hit historic peaks following the Russia/Ukraine conflict, switching volumes collapsed by an estimated 73% to around 1.3 million, according to ElectraLink (opens in new tab) switching data. The non-domestic market was hit particularly hard.

SMEs seeking contracts in late 2022 were quoted electricity rates of 50-60p per kWh - roughly three to four times the pre-crisis baseline. Faced with these numbers, businesses did one of two things:

Some signed. They locked into 1, 2, or 3-year contracts at crisis-era rates, prioritising certainty over value. A business that signed a 36-month deal at 55p/kWh in late 2022 has been overpaying relative to the market for the past two years - and is only now reaching the end of that contract.

Most froze. Switching collapsed because businesses couldn’t stomach locking in at 60p/kWh, but didn’t know what else to do. They let their contracts lapse and fell onto deemed rates - which were also extremely elevated during the crisis period.

Both groups are now arriving at the same place: a renewal decision in a market where rates have dropped significantly from what they were paying.

The Expiration Timeline

The staggered contract lengths create distinct waves:

| Contract Signed | Length | Expires | Status |

|---|---|---|---|

| Q4 2022 | 12 months | Q4 2023 | Already renewed (into a still-elevated market) |

| Q4 2022 - Q1 2023 | 24 months | Q4 2024 - Q1 2025 | First major wave - mostly complete |

| Q4 2022 - Q1 2023 | 36 months | Q4 2025 - Q1 2026 | Expiring now - the final and most expensive cohort |

If you signed a 3-year deal during the crisis, your renewal window is open right now. For a typical SME using 25,000 kWh annually, the savings from renewing at current rates could range from £6,000 to £9,000+ per year, depending on what rate you originally signed at and what you can secure now.

Current Market Rates: What You Can Expect

Here’s how the market has moved:

| Period | Typical SME Electricity Rate | Context |

|---|---|---|

| Early 2021 (pre-crisis) | ~15p/kWh | Stable market baseline |

| Q4 2022 (crisis peak) | 50-60p/kWh | Extreme volatility, illiquidity |

| Late 2025 (pre-tensions) | ~22-26p/kWh | Significantly below crisis peak, elevated above pre-crisis |

| Mid-2026 (current) | Volatile | Middle East tensions causing rapid price swings - rates shifting daily |

Source: DESNZ non-domestic energy price statistics (opens in new tab), ONS industrial energy price indices, independent market data. The late-2025 range is indicative of where the market sat before the current geopolitical volatility. Actual rates vary by business size, region, consumption profile, contract terms, and market conditions at the time of signing.

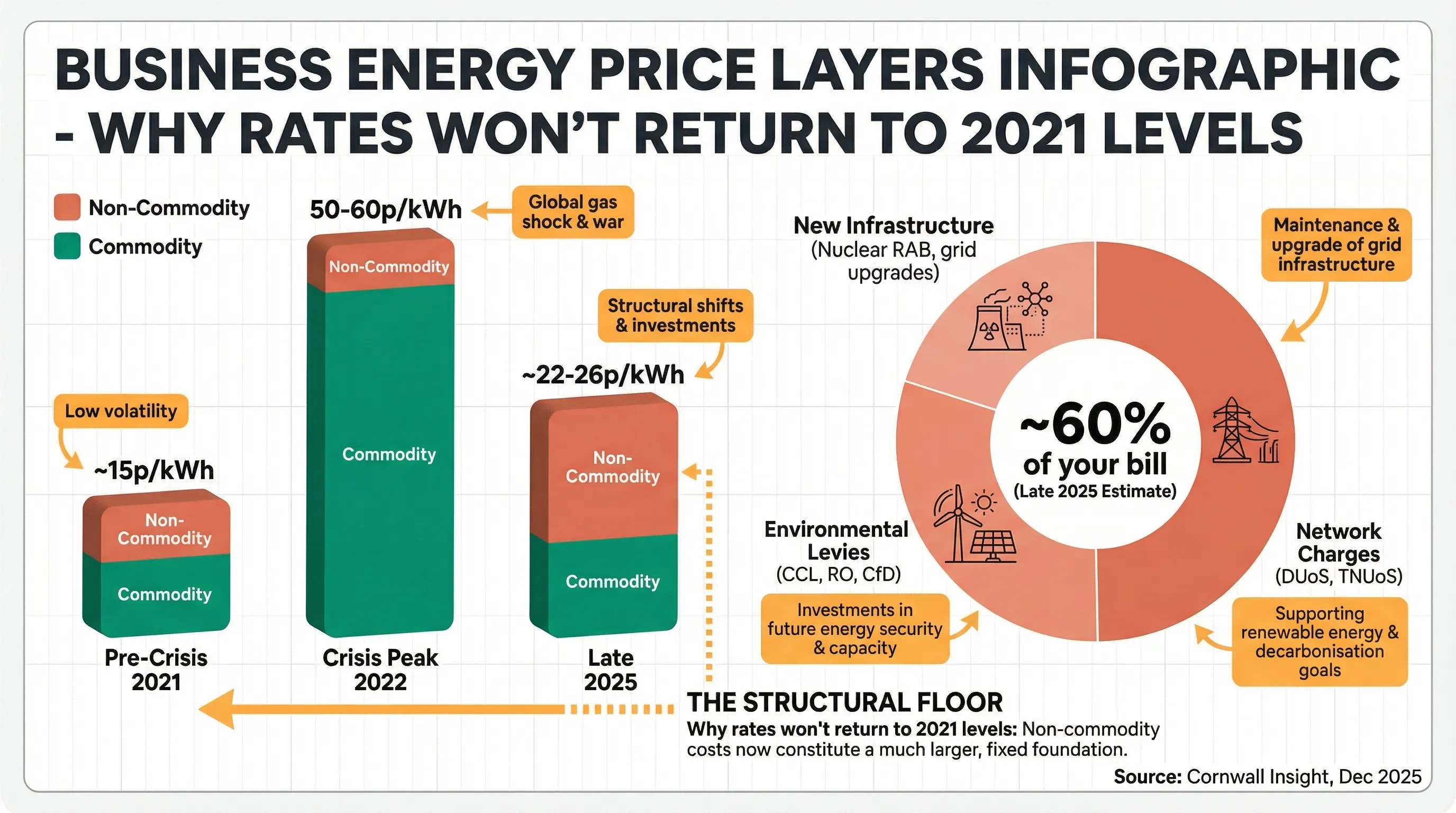

The critical thing to understand: even before the current Middle East volatility, rates were not “back to normal”. The late-2025 indicative range of 22-26p/kWh was still substantially above the pre-crisis baseline of ~15p/kWh - and current volatility may be pushing rates higher still. The reason for the elevated floor is structural.

Why Prices Won’t Go Back to 2021 Levels

Wholesale commodity costs - the price of the actual gas and electricity - have fallen significantly from the 2022 peak. But your bill isn’t just commodity costs. Non-commodity charges now make up an estimated 60% of a typical business electricity bill, according to Cornwall Insight analysis (opens in new tab). The exact proportion varies by consumption band and region. These include:

- Network charges (DUoS, TNUoS) - rising sharply to fund grid upgrades

- Environmental levies (CCL, Renewables Obligation, Contracts for Difference)

- New infrastructure costs - including nuclear RAB charges being socialised into commercial bills

These costs rise independently of wholesale markets. Even if wholesale commodity prices dropped dramatically, non-commodity charges alone would keep your bill close to what you were paying in total before the crisis.

Over the past two decades, each post-shock normalisation has settled at a higher baseline than the one before - though this likely reflects broader trends in infrastructure investment and policy costs as much as crisis-driven ratcheting. Whether this pattern continues depends on how quickly the UK reduces its dependence on globally-traded gas for electricity pricing. Greater domestic renewable generation, battery storage, nuclear capacity, and demand-side flexibility could eventually break the cycle. But that transition is years away - and your contract renewal is happening now. Waiting for prices to “go back to normal” is not a viable strategy for 2026.

RAB and TNUoS Charges: How Suppliers Are Handling Them in 2026

Two specific non-commodity costs are hitting bills right now: the Nuclear RAB Levy (funding Sizewell C construction) and increased TNUoS charges (transmission network costs set by NESO). What makes this particularly important for businesses renewing in 2026 is that suppliers are handling these charges very differently:

The following reflects supplier positions as of April 2026. These may change - check directly with your supplier or broker for the latest position.

- E.ON Next / British Gas - Existing contracts don’t include a separate RAB or TNUoS charge, but standard terms allow regulated charges to be passed through if there are significant market-wide changes. New contracts include forecasted allowances for both.

- EDF Energy - Customers on existing fixed-price contracts will see no price changes despite NESO increasing TNUoS charges. New contracts include forecasted costs.

- Corona Energy - Already increased electricity unit rates by 0.4p/kWh from December 2025 to reflect RAB. TNUoS is included in standing charges from October 2025. No surprises later.

- YU Energy - Nuclear RAB appears as a separate line item on bills from February 2026. TNUoS charges incorporated from February 2026 and reflected in all new quotes.

- Drax Energy - Absorbing the Nuclear RAB Levy for existing Fix Complete or Flex Complete customers in 2026 (position for 2027 not yet confirmed). TNUoS: no price change for existing customers, new contracts include a conservative 50% buffer above published rates.

- Scottish Power - Both RAB and TNUoS are treated as full pass-through charges. TNUoS applies from April 2026, mainly through standing charges. The exact impact varies by region and meter type.

- Smartest Energy - A 0.36p/kWh Nuclear RAB charge applied from December 2025 as a separate line item. TNUoS being applied to some existing contracts from April 2026 where charges have increased significantly beyond what was forecast.

- YGP - Contracts agreed before October 2025: RAB appears as a separate invoice line (estimated 0.4-0.5p/kWh). Contracts after October 2025: RAB included in unit rate.

- SEFE / SSE - Both have RAB and TNUoS already included in pricing. No changes expected for existing contracts.

Why this matters for your renewal: When comparing quotes, you need to know whether RAB and TNUoS are included in the unit rate, added as separate line items, or treated as pass-through charges that could increase mid-contract. A headline rate that excludes these costs looks cheaper but may end up costing more. Ask every supplier explicitly how they treat RAB and TNUoS before you sign.

The New Volatility: Iran and the Middle East

Just as businesses are emerging from the 2022-2023 cycle, a new source of volatility is disrupting the market. Iran-related geopolitical risk - including threats to maritime traffic through the Strait of Hormuz and potential strikes on regional energy infrastructure - is causing significant short-term price swings.

The severity of the impact depends on how the situation develops. In a worst-case scenario involving sustained disruption to Middle Eastern energy infrastructure or shipping routes, wholesale prices could spike significantly - as they did during the early stages of the 2022 crisis. The wholesale forward curve for Summer and Winter 2026 already reflects a geopolitical risk premium.

The practical impact on your renewal:

- Supplier contract offers have shorter validity windows as intra-day price swings make it harder for suppliers to hold rates

- Some businesses are retreating into defensive 3-month contracts rather than committing to longer terms

- Market liquidity is tightening, echoing the early phases of the 2022 cycle

This is Phase 1 of the crisis cycle beginning again - while Phase 3 of the previous cycle is still playing out. The two are overlapping, which makes 2026 uniquely complex but also uniquely important for businesses making renewal decisions.

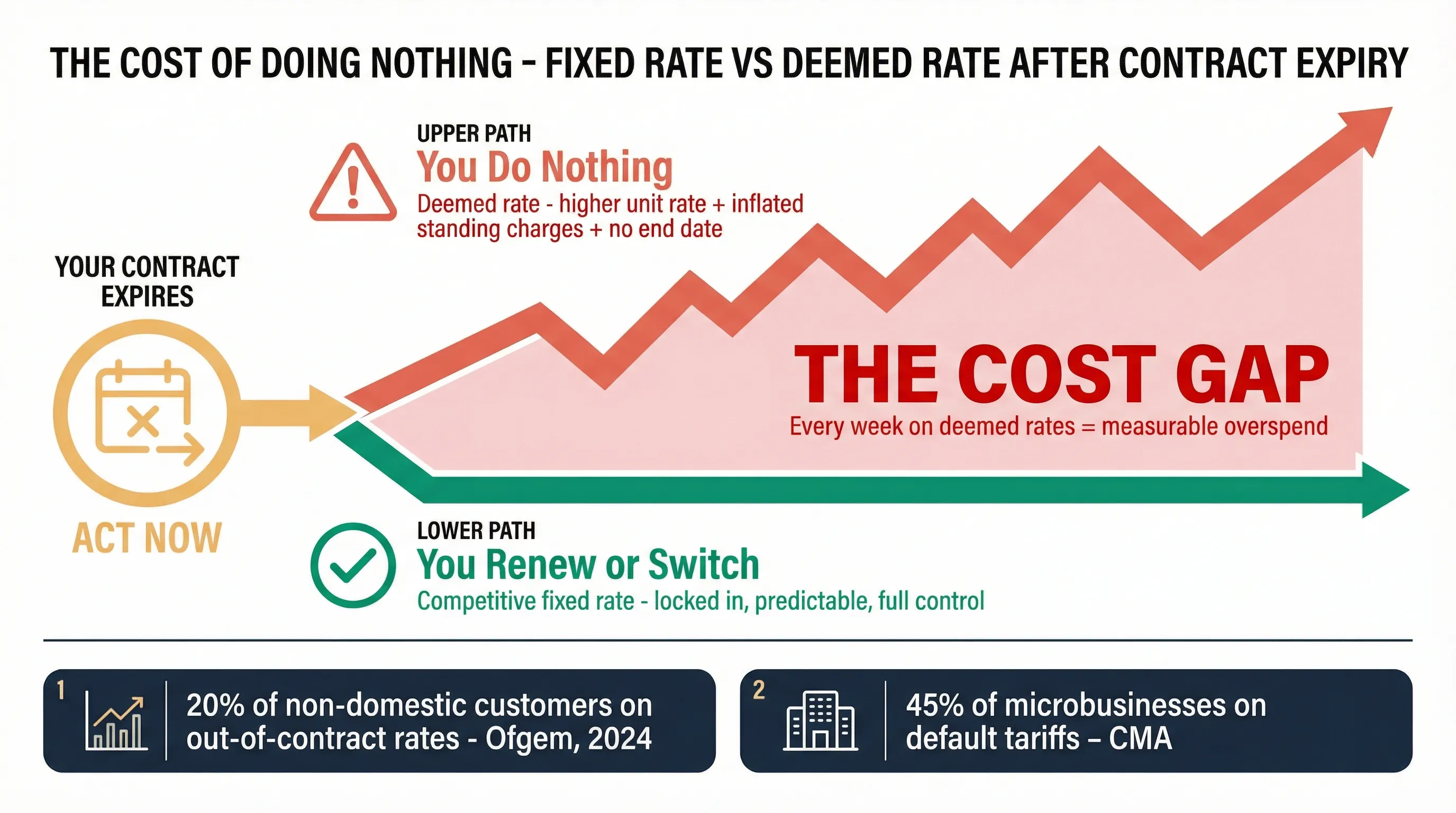

What Happens When Your Business Energy Contract Ends

If your contract expires and you don’t actively renew or switch, your supplier moves you onto their deemed rate - also known as an out-of-contract or default tariff. Business energy deemed rates are typically significantly more expensive than a competitive fixed deal.

Deemed rates vary widely by supplier, with standing charges often significantly higher than on contracted rates. Suppliers are required to publish their deemed rates, but they change periodically and are often buried deep in their websites. Check your supplier’s current deemed rate schedule directly rather than relying on any published comparison - rates shift regularly.

The scale of the problem is enormous. Ofgem’s 2024 survey (opens in new tab) found that around 20% of non-domestic customers were on out-of-contract rates. Among microbusinesses, the problem is even worse - the CMA’s energy market investigation (opens in new tab) found that 45% were on default tariffs, a finding that directly informed Ofgem’s Non-Domestic Market Review.

Many of these businesses fell onto deemed rates during the 2022 crisis - they couldn’t stomach locking in at 60p/kWh, so they let contracts lapse. But the market has moved on. Fixed rates have dropped significantly, yet these businesses are still sitting on deemed rates because they never re-engaged. They’re now paying substantially more than they need to - not because they made a bad decision in 2022, but because they haven’t made any decision since.

Watch Out for Volume Tolerance Clauses

If you signed a crisis-era contract, there’s a sting in the tail that goes beyond the headline unit rate: volume tolerance.

When you sign a fixed contract, your supplier immediately buys your forecasted energy volume on the wholesale forward market. Volume tolerance sets a band - typically 80-120% of that forecast - within which the fixed rate applies. Go outside the band, and penalties kick in.

During the crisis, something perverse happened. Faced with 50-60p/kWh rates, businesses cut consumption aggressively - reducing hours, turning off equipment, pausing production. Their usage dropped below the 80% floor of their volume tolerance band. The supplier, left holding energy pre-purchased at crisis peak prices that could only be sold back at a loss, enforced the penalty clauses.

The result: businesses faced additional charges for reducing their energy consumption during a national crisis. The suppliers had a contractual right to enforce the clause - they’d hedged at the agreed volume - but for SMEs, the outcome felt deeply unfair.

Reports of volume tolerance enforcement increased during 2023-2024 as businesses that had cut consumption during the crisis fell below their contracted tolerance bands. Energy Ombudsman complaints about commercial energy rose 112% in 2024 - driven by a combination of volume tolerance disputes, broker commission complaints, and billing issues from the crisis period.

When renewing, negotiate the widest volume tolerance band possible. Some suppliers offer contracts with wider tolerance bands or flexible volume arrangements - ask specifically about volume tolerance terms before signing, especially if your business has variable or seasonal energy usage.

What Energy Analysts Recommend for 2026

The 2026 market presents a genuine tension: lock in now for certainty, or wait for projected price drops?

The Case for Fixing Now (12-24 Months)

Current fixed rates represent a major improvement over crisis-era contracts. Iran-related volatility could push prices higher in the short term. A 12-24 month contract provides immediate protection while keeping you free to re-enter the market in 2027-2028.

The Case for Waiting

Global LNG supply is projected to surge significantly between 2025 and 2027. This influx should ease wholesale commodity prices further. Businesses that lock into 36-month contracts now risk missing this structural price drop.

The Prevailing Consensus

Most energy procurement specialists recommend 12-24 month contracts for SMEs renewing in 2026. This duration protects you from unpredictable geopolitical volatility today while ensuring you’re not locked in too long if prices drop as projected.

The consensus among procurement specialists is clear: doing nothing is the worst option. The gap between a competitive fixed rate and a deemed rate is too large to justify inaction under any realistic market scenario.

When to Renew Your Business Energy Contract

The sweet spot for starting your renewal is 3-6 months before your contract expires. Too early (12+ months out) and suppliers often add a risk premium because they’re hedging further into an uncertain forward curve. Too late (final few weeks) and you’re exposed to whatever the short-term market is doing - and you risk defaulting onto deemed rates if the process overruns.

At 3-6 months, suppliers have enough lead time to hedge your volume efficiently without pricing in excessive uncertainty. You also have time to compare multiple offers rather than accepting the first quote under pressure.

If your contract expires in the next 6 months, start looking now. If it’s already expired, you’re on deemed rates and can switch immediately with no exit fees. Either way, every week of delay has a measurable cost.

What’s Changed Since the Last Crisis

The market you’re renewing into is fundamentally different from the one you left. Several structural changes now work in your favour:

Stronger Regulation

Ofgem’s Non-Domestic Market Review (opens in new tab) introduced major protections:

- Expanded Ombudsman access - since December 2024, small businesses (not just microbusinesses) can access the Energy Ombudsman for free dispute resolution

- Standards of Conduct - since July 2024, suppliers must treat businesses of all sizes fairly, honestly, and transparently (previously only applied to microbusinesses)

- Deemed rate governance - Ofgem now requires that deemed rates must not “significantly exceed” the actual cost of supply

Broker Transparency

The TPI Code of Practice and enhanced Ofgem regulation now require explicit disclosure of broker commissions. You have the right to know exactly how much of your rate is going to a middleman. If your broker won’t disclose their fee, that tells you everything you need to know. Read our guide on how broker uplift works before signing anything.

Half-Hourly Settlement (MHHS)

The rollout of Market-wide Half-Hourly Settlement (MHHS) is migrating all electricity meters to 30-minute interval measurement by May 2027. For businesses renewing now, this means:

- More accurate pricing - suppliers get granular data on when you use power, reducing their forecasting risk and potentially lowering your rate

- New product types - time-of-use tariffs that reward shifting consumption to off-peak hours are becoming available

- Profile classes are being phased out - replaced by Standard Settlement Configuration codes that reflect actual usage patterns

What to Do Right Now

If your crisis-era contract is expiring in the next 12 months:

- Find your contract end date (it’s on your bill, or call your supplier)

- Start comparing rates now - don’t wait until the last month

- Compare total annual cost, not just the headline unit rate

- Check the volume tolerance band before signing anything

- Aim for a 12-24 month contract in the current market

- Read the contract red flags guide before you sign

If your contract has already expired and you’re on deemed rates:

You can switch immediately with no exit fees. There is no reason to stay on deemed rates for a single day longer than necessary. Learn how to switch in 20 minutes.

If you’re not sure what you’re on:

Check your bill for the tariff name. If it says “Standard Variable”, “Deemed”, “Out of Contract”, or anything with “Freedom” or “Flexible” in the name, you’re likely on deemed rates. If you’re unsure, compare your current unit rate against recent fixed-rate quotes - if there’s a significant gap, you may be on a deemed rate or paying a high broker uplift.

Ready to switch? Compare transparent energy quotes or join the Meet George platform waitlist to switch in 20 minutes with full cost transparency - our flat 1p/kWh fee is shown separately, so you always know exactly what you’re paying.