TL;DR: Key Takeaways

Energy broker consolidation - the structural reduction in the number of independent TPIs operating in the UK market - appears to be accelerating. The UK has roughly 2,700 energy brokers. Within three years, somewhere between 500 and 1,000 of them could be gone - absorbed, insolvent, or simply closed. That is the direction the evidence points when you look at three structural forces hitting the market simultaneously: mandatory government regulation appointing Ofgem as the direct regulator, technology that is making manual brokerage increasingly obsolete, and a Supreme Court precedent that has turned historical commissions into legal liabilities. The survivors will be larger, more transparent, and more useful. Most of the casualties will be small operations that built their business on opacity.

Key Statistics

| Metric | Figure | Source |

|---|---|---|

| Estimated UK energy brokers | 2,700+ | Energy Ombudsman register |

| TPI Code of Practice adoption | 52 signatories (<2%) | RECCo, Jan 2026 |

| Ombudsman complaint growth | 112% YoY (1,568 cases) | Energy Ombudsman, 2024 |

| Sales-related disputes | 88% of all cases | Energy Ombudsman, 2024 |

| Cases upheld in customer’s favour | 58% | Energy Ombudsman, 2024 |

| Domestic PCW market today | 11 accredited sites | Ofgem Confidence Code |

| Mandatory Ofgem registration | Expected 2027-2028 | DESNZ, Oct 2025 |

The Three Forces Driving Consolidation

We’re a TPI ourselves - we operate in this market, not on the sidelines - so we’re watching these developments closely. What follows is our reading of the public evidence.

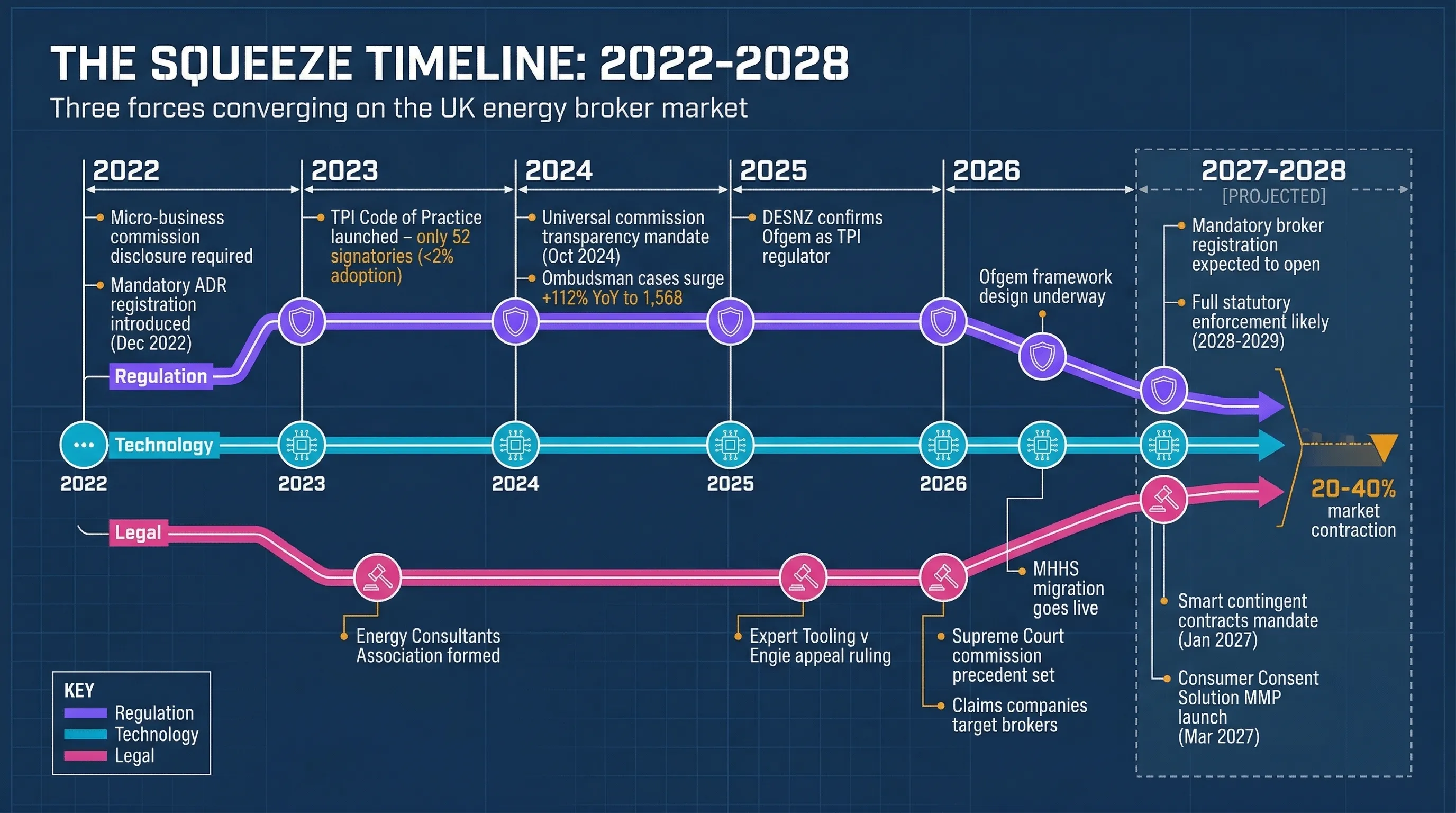

The UK business energy broker market has operated for over a decade with uniquely low barriers to entry - and that is the core reason energy broker consolidation now looks inevitable. No licence required. No mandatory transparency. No direct regulator. That appears to be changing - and when it does, the market seems likely to contract significantly.

Three forces are converging:

- Regulation - The government has confirmed Ofgem will become the direct regulator for brokers, with mandatory registration expected from 2027-2028 and industry-funded compliance costs

- Technology - Market-wide Half-Hourly Settlement is replacing manual data processes with digital systems that many small brokers will struggle to implement without in-house technical skills

- Legal liability - A Supreme Court precedent has weaponised historical commission practices, creating retroactive exposure that could bankrupt undercapitalised firms

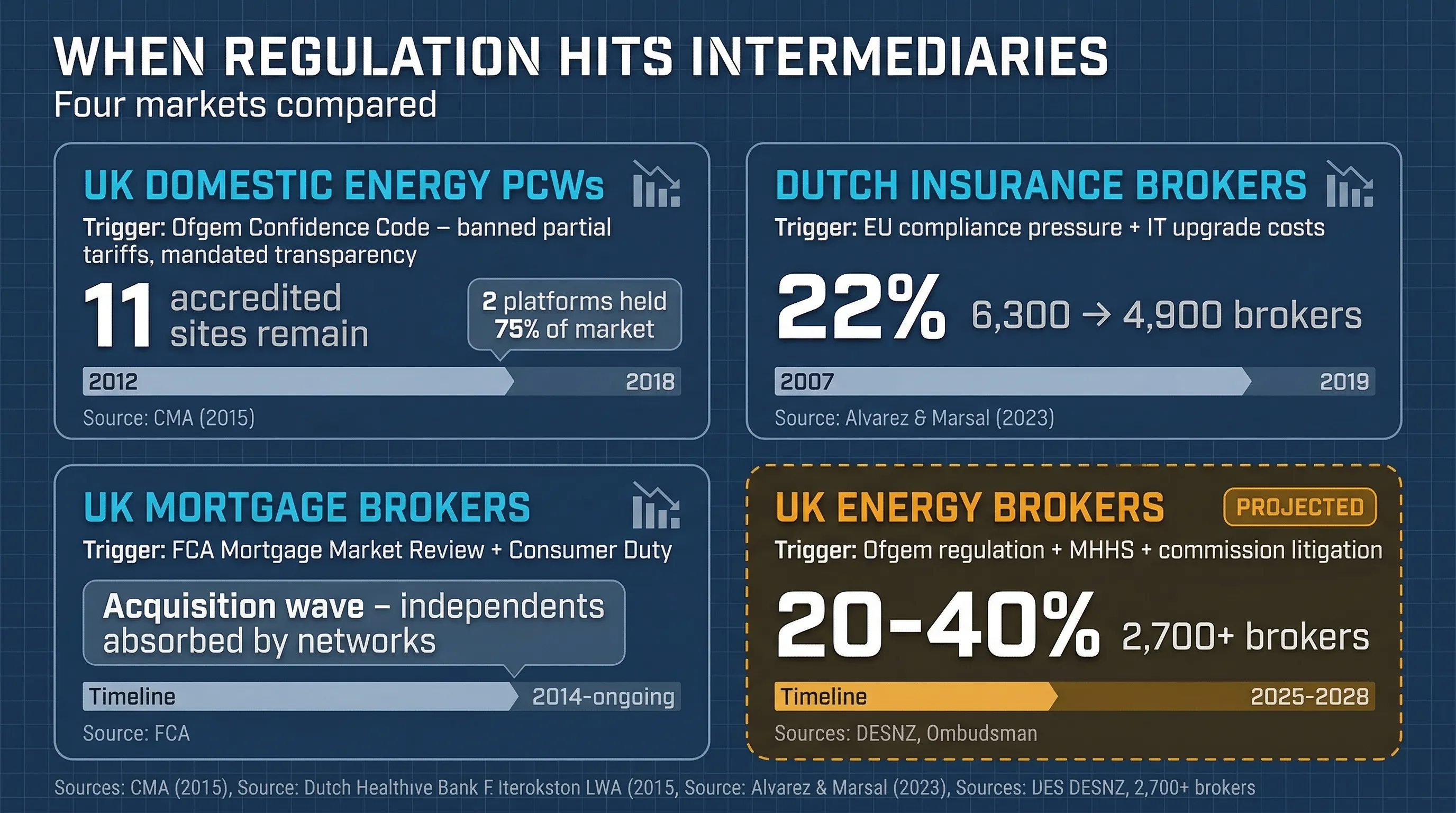

Each of these alone would cause market disruption. Together, they suggest a contraction of 20-40% may be likely - consistent with what happened in other intermediary markets that went through a similar transition.

How Big Is the Broker Market Today?

Mapping the exact size of the UK energy broker market is difficult because there has never been a mandatory licencing register. But cross-referencing available data gives us a reasonable picture.

The estimated total population sits at approximately 2,700+ individual entities, ranging from multinational consultancies to sole traders running telephone sales desks. The Energy Ombudsman is the largest ADR provider - brokers must register with an ADR scheme to work with most suppliers - and its downloadable register (opens in new tab) currently lists over 2,700 active brokers. During the scheme’s second year (December 2023 to November 2024), the Energy Ombudsman’s annual report (opens in new tab) recorded 1,819 registered brokers, so the market appears to have grown since then - though some brokers may be registered with alternative ADR providers.

Revenue distribution follows a severe Pareto curve - a small number of players capture a disproportionately large share of the total market, while the long tail of smaller operators share what is left. A small number of large enterprises - firms like those tracked by Cornwall Insight’s TPI rankings - capture a disproportionate share through economies of scale and sophisticated data platforms. The vast majority of registered brokers are small operations reliant on manual processes and simple uplift commissions embedded in the customer’s unit rate.

Force 1: Regulation Is Coming - And Brokers Will Pay for It

The DESNZ Mandate

In October 2025, the Department for Energy Security and Net Zero published its official response (opens in new tab) confirming that Ofgem will become the direct regulator for energy brokers. This is not a consultation. It is a confirmed policy direction awaiting parliamentary time.

The indicative timeline, subject to parliamentary time:

- 2026: Ofgem designs the regulatory framework and conducts market surveys

- 2027-2028: Mandatory broker registration expected to open

- 2028-2029: Full statutory enforcement likely to follow

The critical detail buried in the DESNZ response: the cost of regulation will be recovered directly from the TPI sector through annual fees. The government explicitly rejected the alternative of recovering costs through energy suppliers, reasoning that this would unfairly burden all energy consumers - similar to how non-commodity costs like network charges are currently recovered by suppliers and passed through to end users’ bills.

For a large brokerage with substantial revenue, annual licence fees will likely be a rounding error. For a small broker operating on thin margins - and industry sources suggest as many as 70% of brokers generate less than £200,000 per year in revenue - these new fixed overheads could be fatal. Licence fees, compliance officers, reporting systems, and professional indemnity insurance all represent permanent cost increases that cannot easily be passed to customers in a competitive market.

Self-Regulation Already Failed

The incoming statutory regulation is a direct consequence of the industry’s failure to regulate itself. In October 2023, RECCo introduced the voluntary TPI Code of Practice - a transparency framework requiring signatories to disclose how they are paid, show all quotes to customers, and maintain robust complaints procedures.

As of January 2026, only 52 out of approximately 2,700+ brokers had signed. That is less than 2% adoption after more than 20 months.

The reluctance appears commercially rational, if concerning. Traditional broker models rely on undisclosed commissions - a 2-4p/kWh margin embedded in the unit rate that the customer never sees. Voluntarily disclosing this erodes the informational advantage that sustains the business. The shift from a voluntary code to a mandatory licence will strip away this opacity, and the 98% non-adoption rate suggests a significant portion of the market may have built their business model around it.

Complaints Are Surging

The Energy Ombudsman’s data from its second-year broker scheme report (opens in new tab) quantifies the scale of market failure:

- Accepted cases surged 112% year-on-year to 1,568

- 88% of disputes were sales-related - not service delivery issues

- 58% of cases were upheld in the customer’s favour

- The signposting rate (brokers telling customers about their right to escalate) was just 8%

Every upheld complaint costs the broker money - compensation, case fees, and sometimes forfeited commissions. As awareness of the ADR route grows among UK businesses, dispute volumes will likely continue rising. For small brokers, complaints are transitioning from a rare anomaly into a recurring cost centre.

Force 2: Technology Is Making Manual Brokerage Obsolete

Half-Hourly Settlement Changes Everything

Market-wide Half-Hourly Settlement (MHHS) is the most significant overhaul of UK electricity settlement processes in decades. It requires all electricity meters to be settled on half-hourly data rather than estimated annual profiles. (Gas settlement is unaffected by MHHS, but brokers who handle both fuels - which is most of them - still face the full impact on the electricity side of their business.)

Migration is already underway. Sprint 1 ran from February to March 2026, primarily covering domestic meters, with over two million meters transitioned to half-hourly settlement. Non-domestic migration begins in earnest with Sprint 2 from April 2026.

For brokers, this will fundamentally change how quotes work. The traditional model - pull an Estimated Annual Consumption (EAC) figure, ring or email a few suppliers, and send back a PDF or spreadsheet to the customer - is becoming increasingly outdated. As meters migrate to half-hourly settlement, brokers who want to access time-of-use tariffs from suppliers will need to pull half-hourly consumption data instead.

Much of this is still being worked out. Currently, brokers access EAC data through ElectraLink (opens in new tab). As MHHS rolls out, consumption data from the Data Communications Company (DCC) (opens in new tab) will increasingly flow through the Data Integration Platform (DIP) (opens in new tab), run by Elexon (opens in new tab). The EAC is still useful today, but it is becoming more deprecated with each migration sprint. Layered on top of all this is the emerging Consumer Consent Solution (opens in new tab), which governs how customers grant access to their energy data to third parties including brokers.

The Technology Investment Gap

Accessing this data is not free. Third-party data providers offer tiered API pricing where costs per data call decrease at higher volumes. Large brokerages with thousands of active clients can amortise these costs across their portfolio and generate instant, automated quotes. Small brokers making a handful of API calls per day pay substantially more per query - and they still need the software infrastructure to process the data.

This creates a self-reinforcing cycle. Larger brokers invest in technology, quote faster, win more clients, and spread costs further. Smaller brokers, lacking the in-house technical skills to build these integrations - and facing significant costs to outsource them - fall behind on speed, accuracy, and customer experience. The cost of merely accessing the data required to do the job begins to exceed the potential commission.

Some data providers are responding by building portal-based (non-API) products for smaller brokers who cannot integrate APIs - but this is a stopgap, not a solution. A broker manually logging into a portal to pull half-hourly data for each customer cannot compete with a platform that does it automatically at scale.

Digital Consent Is Replacing Paper LOAs

The shift to digital data access brings stricter consent requirements. The traditional Letter of Authority (LOA) - a PDF emailed between parties - is fundamentally incompatible with secure API data gateways. The industry is moving toward digital consent models with auditable verification trails.

Implementing secure digital consent portals requires further technology investment, raising the barrier to entry yet again. The direction of travel is clear: the technical infrastructure required to operate as an energy broker in 2028 will look nothing like what was required in 2022.

Force 3: The Legal Time Bomb

Expert Tooling v Engie

The most acute existential threat to mid-market brokers is the explosion of civil litigation around “secret” and “half-secret” commissions. This was crystallised in Expert Tooling and Automation Ltd v Engie Power Ltd (opens in new tab), settled by consent in the Supreme Court in January 2026.

The facts were straightforward. Expert Tooling used a broker (Utilitywise) to secure an electricity contract with Engie. The client knew the broker was receiving some commission from the supplier but did not know the exact amount, the calculation method, or that the cost was passed to them via a higher unit rate. The Court of Appeal ruled this constituted a “half-secret” commission - a breach of fiduciary duty. Crucially, the court ruled that the client’s commercial sophistication was irrelevant. Brokers cannot assume a large business “should have known” how energy commissions work.

The Implications Are Industry-Wide

This precedent creates three cascading problems:

- Retroactive liability - Brokers and the suppliers who paid them are vulnerable to claims seeking recovery of all commissions paid on historical contracts where explicit mathematical disclosure was not provided

- Claims management companies - Professional litigation firms are actively targeting the business energy sector, using the Expert Tooling precedent to aggregate thousands of claims

- Insolvency as the path of least resistance - In the original case, the broker (Utilitywise) had already entered administration. Smaller brokers facing a wave of claims may choose voluntary liquidation over years of tribunal defences

The financial stability of the intermediary supply chain is arguably compromised by this precedent. Brokers who operated transparently have nothing to fear. But brokers who relied on opacity - and the low TPI Code adoption rate suggests there may be many - face potentially significant historical liability.

Smart Contingent Contracts Add Further Pressure

From 1 January 2027, DESNZ’s smart-contingent contracts policy (opens in new tab) will bar energy suppliers from entering new fixed-term contracts with business customers unless the customer has, or agrees to install, a smart meter. Brokers will bear the administrative friction - navigating installation logistics, managing customer objections, and ensuring compliance before a commission-generating contract can be signed. This adds complexity, delays sales cycles, and increases the cost of acquiring each customer.

Historical Precedent: This Has Happened Before

The projected 20-40% contraction is not without precedent. It aligns with what we have observed in comparable intermediary markets when regulation, transparency, and technology converged.

Domestic Energy Switching

Before 2015, the domestic energy price comparison website (PCW) market was fragmented. Following Ofgem’s Confidence Code - which banned partial tariff views and mandated commission transparency - the market rapidly consolidated. By 2015, just two platforms (uSwitch and MoneySuperMarket) held approximately 75% of the market. Today, the Ofgem Confidence Code accredited list features only 11 major switching websites (opens in new tab).

The pattern suggests that strict regulatory standards tend to favour well-capitalised tech platforms that can absorb compliance costs and invest in infrastructure. Smaller, undifferentiated intermediaries tend to get squeezed out.

UK Mortgage Brokers

The mortgage market went through a similar transformation after the FCA’s Mortgage Market Review and Consumer Duty rules. The compliance burden - documentation requirements, continuous professional development, reporting systems - drove a wave of acquisitions. Smaller independents were absorbed by larger networks to pool compliance costs and share technology infrastructure. The total number of independent brokerages declined while the surviving firms grew larger and more sophisticated.

European Insurance Brokers

Perhaps the most instructive parallel comes from the Dutch insurance brokerage market. According to Alvarez & Marsal’s global insurance brokerage report (opens in new tab), the Dutch market contracted by 22% - from roughly 6,300 brokers in 2007 to 4,900 in 2019.

The cause was not falling demand. Total premiums remained stable. The contraction was driven by “growing compliance pressure on companies, requiring investments that companies are not inclined to make given their own management horizon.” When faced with IT upgrades to meet European transparency laws, smaller proprietors chose to sell their portfolios or exit entirely.

With DESNZ regulation on the horizon and Consumer Consent Solution integration becoming essential to access half-hourly data, hundreds of UK energy broker proprietors appear to face the exact same calculation.

The Counter-Argument: Won’t Regulation Help Good Brokers?

It is worth stating the strongest counter-argument honestly: regulation could grow the market for surviving brokers.

According to the Energy Ombudsman’s sector outlook, while 25% of surveyed brokers viewed regulatory change as a significant challenge, a majority of 56% believed regulation would actually help their business. The logic is sound. Removing rogue operators restores consumer trust. Higher trust drives higher engagement from the millions of SMEs who currently avoid brokers entirely. The total addressable market expands.

There is also a genuine opportunity in the net-zero transition. As businesses face mounting pressure to decarbonise, there is growing demand for complex advisory services - PPAs, demand-side response, EV fleet charging, carbon reporting - that go far beyond simple energy procurement. Brokers who evolve from transactional sales operations into genuine energy consultancies will thrive.

But this evolution requires capital, skilled staff, and sophisticated technology - precisely the resources that many smaller brokerages may lack. The value of surviving brokerages will likely increase. The number of independent market entities will decrease. Both things can be true simultaneously.

What This Means If You Use a Broker

If your business currently uses an energy broker, this consolidation does not necessarily mean you need to act immediately. But it does mean you should:

- Check whether your broker has signed the TPI Code of Practice - the voluntary transparency code that only 2% of brokers have adopted. If they have not, ask why not.

- Request commission disclosure upfront - since October 2024, broker commissions must be disclosed in the contract. Ask your broker to state their fee upfront before you sign, and verify the specific rate in p/kWh and total value in pounds appears in the contract.

- Know your ADR rights - if you have a dispute, your broker has 8 weeks to resolve it before you can escalate to the Energy Ombudsman. Businesses with fewer than 50 employees can use this route.

- Consider whether you need a broker at all - the market is moving toward self-service platforms where you can compare supplier rates directly, with transparent fees and no cold calls.

Where We Stand

As a TPI subject to the same incoming regulation, we have a stake in this. We think the market is moving toward transparency and self-service - and we have built accordingly. But many of the brokers who will exit the market are small business owners who built legitimate operations under the rules that existed at the time. The squeeze is structural, not personal.

Sources: DESNZ government response (October 2025), Energy Ombudsman second-year broker scheme report (June 2025), Weightmans legal analysis of Expert Tooling v Engie (January 2026), CMA price comparison website data (2015), Alvarez & Marsal global insurance brokerage report (2023). All source links verified as of March 2026.