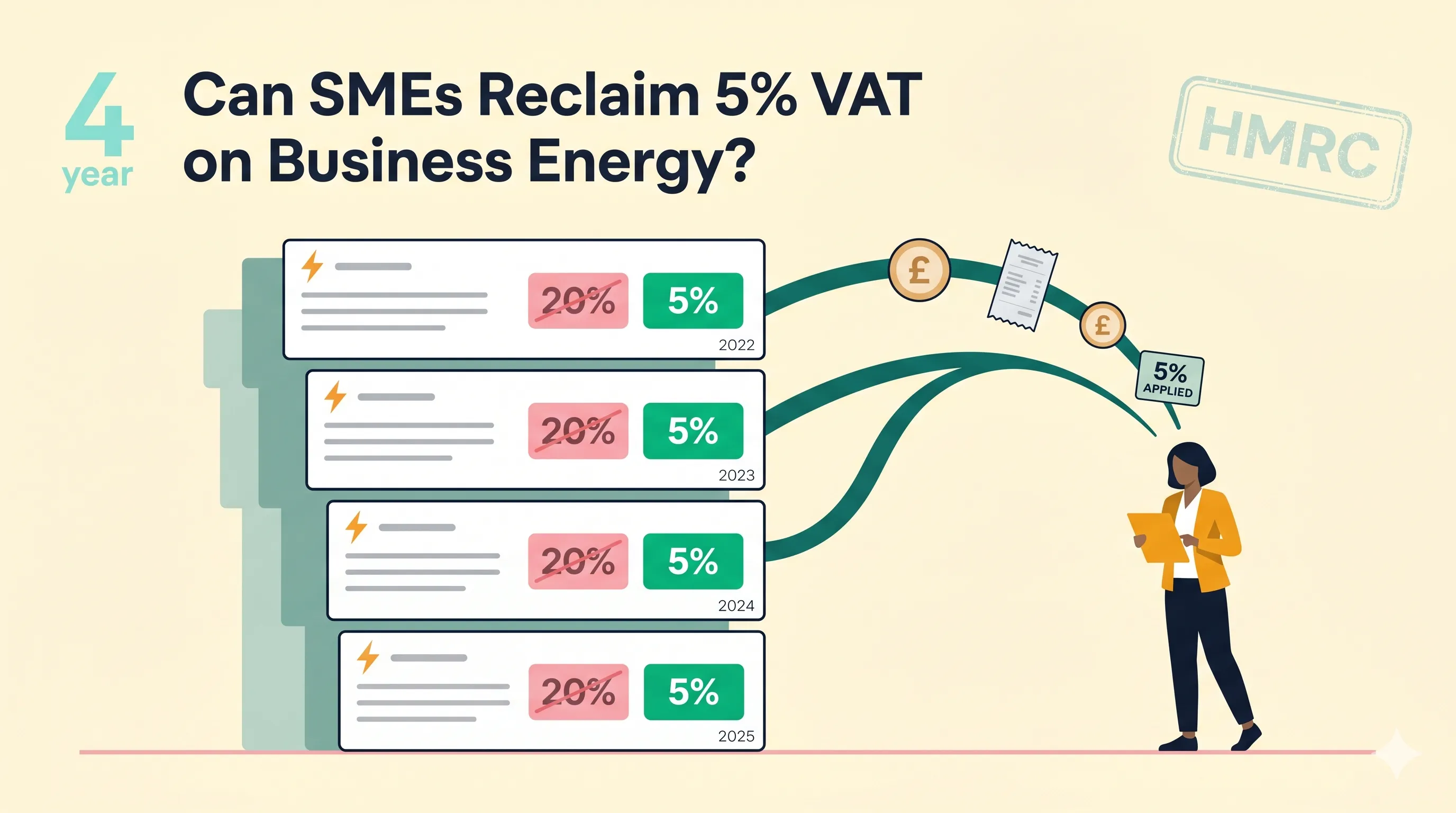

Quick answer: Yes. If your business genuinely qualifies for the reduced 5% VAT rate on energy but has been charged the default 20%, you can ask your supplier for a refund of up to 4 years of overpaid VAT. The supplier - not HMRC - processes the refund. You need a signed VAT declaration certificate, evidence of your qualifying status, and a written request that explicitly asks for the backdated correction. The escalation route if there is a dispute is the Energy Ombudsman.

For most SMEs that qualify, the reclaim sits in the £1,500-£5,000 range per meter, per 4-year cap. It often goes unclaimed because the customer (not the supplier) is responsible for declaring qualifying status - so reclaims only happen when a business knows to ask.

TL;DR

- Yes, 4 years is reclaimable. HMRC’s 4-year window applies to energy VAT errors. Suppliers must honour it.

- The supplier processes the refund, not HMRC. Your job is to give them watertight evidence and a specific figure.

- Three escalation steps if they refuse: formal complaint (8 weeks), Energy Ombudsman (free + binding), or HMRC error correction via VAT Notice 700/45 (opens in new tab) (VAT-registered only).

- Switched supplier? You still claim from whoever overcharged you - the 4-year window runs from each original bill, not from your current relationship.

- VAT-registered? You probably already reclaim through returns. The 5% rate still matters for cashflow, Climate Change Levy exemption, and Flat Rate Scheme businesses.

If you have not yet checked whether you qualify, start with our master guide: VAT on Business Energy: 5% vs 20% Rules Explained. This article assumes you already know you qualify - and focuses on the action.

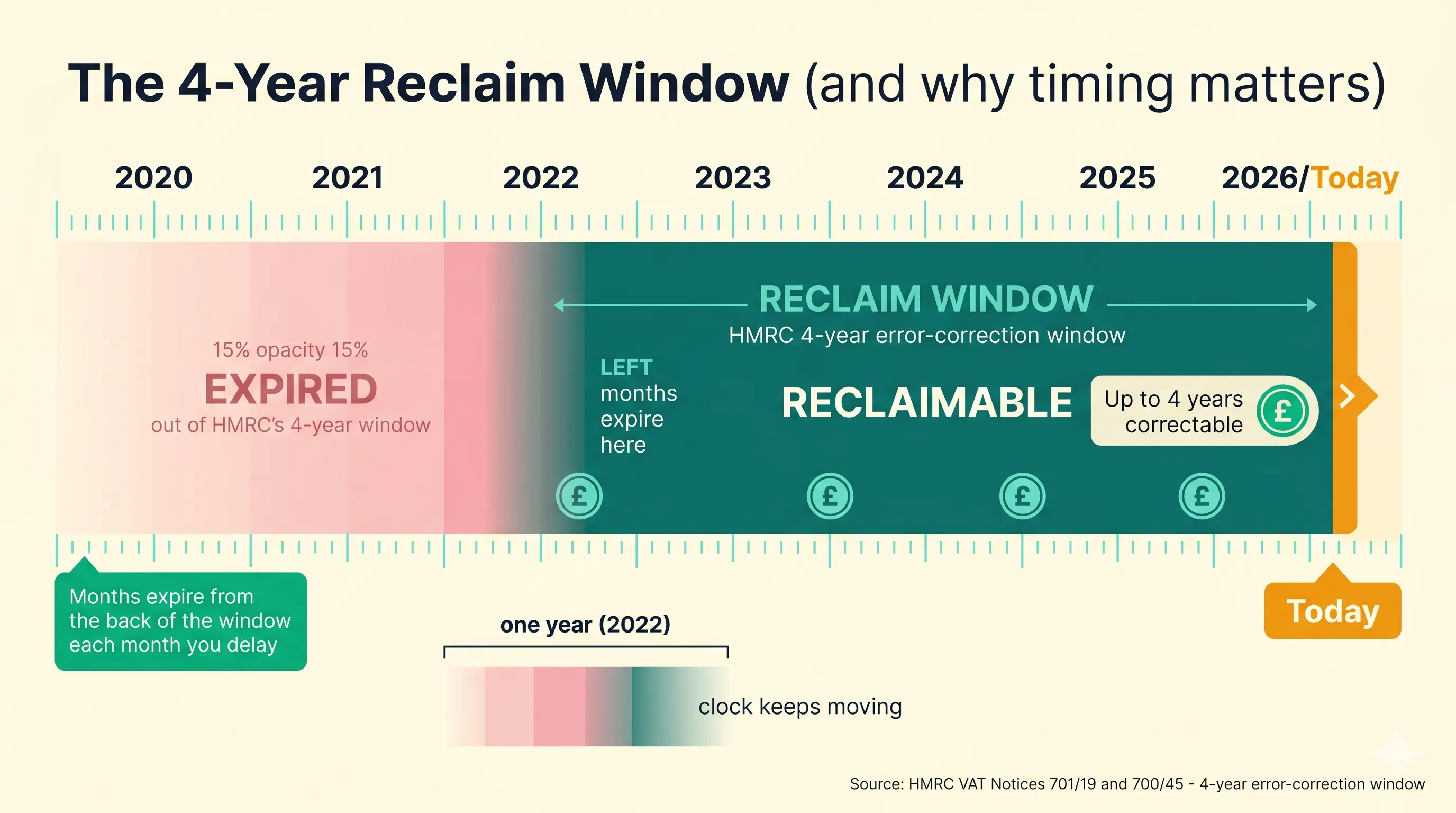

The 4-Year Rule (and Why It Matters Now)

HMRC caps VAT error corrections at 4 years from the date of the overpayment. That is the legal ceiling - and it applies regardless of why the 20% rate was being charged in the first place. Suppliers correctly default to 20% on business meters until the customer submits a VAT declaration showing qualifying use. The reclaim mechanism exists precisely because customers who were always eligible often only get around to declaring later.

HMRC’s own position (VAT Notice 700/45 (opens in new tab)): “If you think you have been wrongly charged an amount as VAT by your supplier, you should seek a refund from your supplier. If you overpaid your supplier and your supplier accounted to HMRC for a corresponding amount, they can make a refund claim to HMRC in order to reimburse you.”

For a qualifying SME, four years of 15% overcharging on a £5,000 annual electricity bill is £3,000. On a £10,000 bill it is £6,000. Multiply by every meter you operate.

Two reasons this is urgent:

- The clock keeps moving. Every month you delay, the oldest month of your reclaim falls off the back of the 4-year window. If you were overcharged from May 2022 onwards and you file in May 2026, you get the full window. File in August 2026 and you lose three months of reclaim.

- Backdating is a separate request from the going-forward change. Some suppliers will apply the 5% rate from the date your declaration is received and treat that as the full remedy. If you were eligible for the earlier period, you can ask for that to be corrected too - HMRC’s framework treats earlier overcharging as an overpayment of VAT eligible for the 4-year error-correction window, not a discretionary credit. You need to ask for it explicitly.

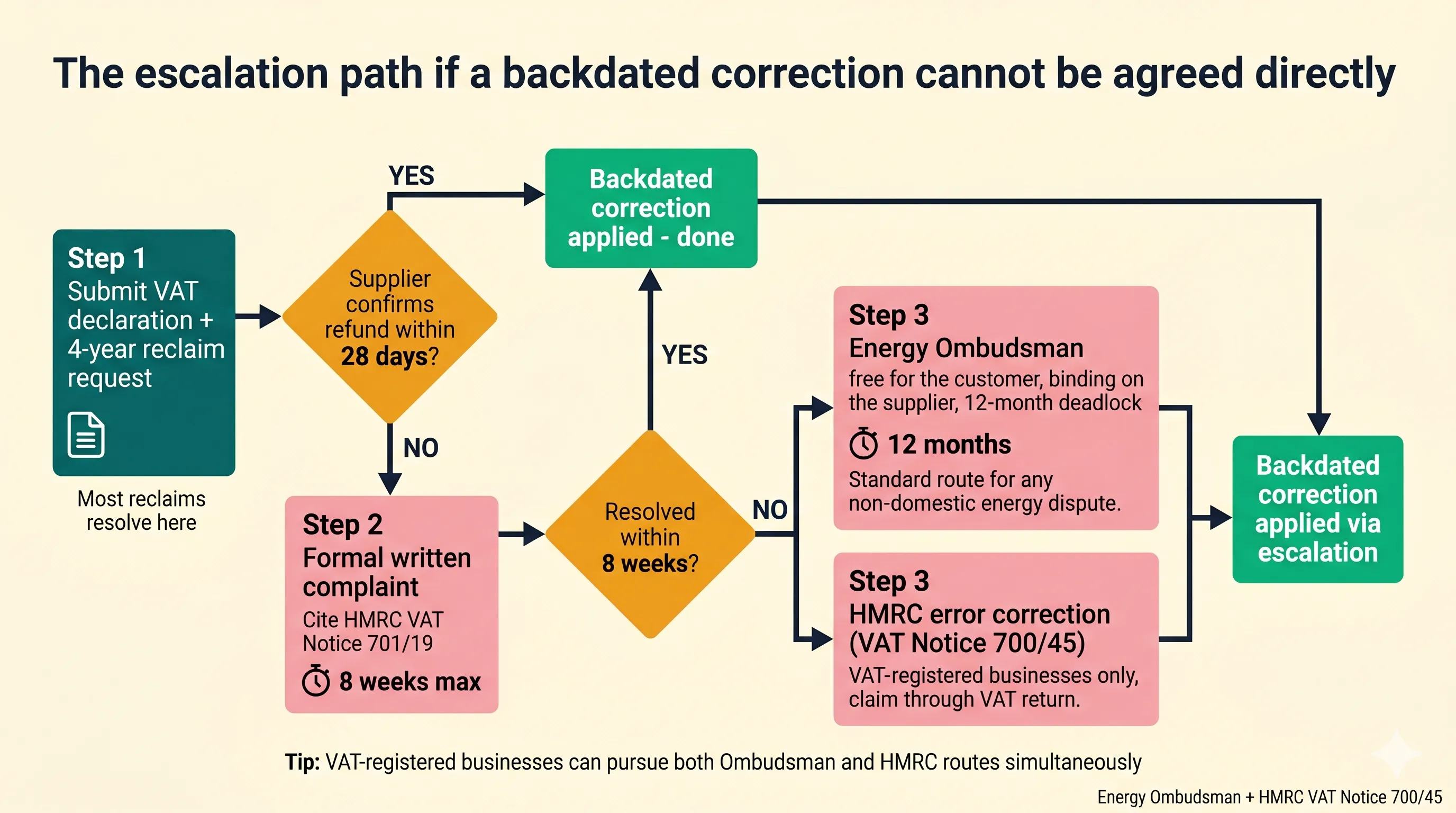

If the supplier and customer cannot resolve a backdating dispute directly, the standard non-domestic escalation route is the Energy Ombudsman (opens in new tab), which is free for the customer and binding on the supplier.

Quick Eligibility Check

You qualify for 5% VAT if any one of the following applies:

- De minimis: Less than 1,000 kWh/month of electricity (33 kWh/day, 12,000 kWh/year), or less than 4,397 kWh/month of gas (145 kWh/day, 52,764 kWh/year). Most micro-businesses, small retail units, salons, and home-office set-ups fall under this without realising it.

- Charity (non-business activities): Energy used for fundraising, worship, or community services.

- Residential or quasi-residential: Care homes, holiday lets, student halls, places of worship.

- Mixed-use 60% rule: If 60% or more of your energy is used for qualifying purposes (residential or charitable), the entire supply qualifies for 5%. Below 60%, you can apportion.

Full breakdown of eligibility tests, qualifying activities, and the 60% rule is in the master post: VAT on Business Energy: 5% vs 20% Rules Explained.

The 5-Step Reclaim Process

Step 1: Verify Eligibility and Gather Evidence

Pull at least 12 months of meter readings and bills. If you are claiming under de minimis, the threshold is monthly - not annual - so a single high-consumption month can break eligibility. Suppliers will check this when reviewing the claim.

| Qualifying route | Evidence needed |

|---|---|

| De minimis | 12+ months meter readings showing average below threshold |

| Charity | HMRC charity reference number + written declaration of non-business use |

| Residential / care / holiday lets | Lease, ownership documents, or licensing for the use type |

| Mixed-use (60%+) | Floorplan or schedule showing qualifying percentage |

Estimates are usually rejected. Exact figures with backup evidence get through faster.

Step 2: Calculate the Overpayment

The maths is simple: 15% of the net (ex-VAT) energy bill, per year, per meter.

Worked example for a small office:

- Annual electricity bill (ex-VAT): £4,200

- VAT charged at 20%: £840

- VAT that should have been charged at 5%: £210

- Annual overpayment: £630

- Cap at 4 years: £2,520 reclaim

Add gas separately. Add other meters separately. Document every figure. Suppliers will not accept a single round number with no working - they want the calculation per billing period, ideally pulled from your actual bills. Spreadsheet attached to your reclaim request.

Step 3: Submit a VAT Declaration + Backdated Reclaim Request

Two things need to happen at the same time:

- A VAT declaration certificate. This is the standard form your supplier uses to apply 5% going forward. Each supplier has its own version - search “[supplier name] VAT declaration certificate” or call their business team.

- A written backdated reclaim request. The declaration on its own only changes the rate going forward; the backdated correction is a separate ask. Submit both together and make the backdated part explicit: “I am also requesting a refund of overpaid VAT for the past 4 years, totalling £X across this meter, in line with HMRC’s 4-year error correction window under VAT Notice 701/19 (opens in new tab).”

Send by email and keep the trail. If the supplier provides a portal, upload through the portal and email a copy.

Copy-and-Paste Email Template

Subject: VAT reclaim request - Account [your account number], MPAN [your MPAN]

Dear [Supplier Business Team],

I am writing to request a refund of overpaid VAT on the above account

for the period [start date, max 4 years back] to [today's date]. My

business qualifies for the reduced 5% VAT rate under [de minimis /

charity / residential / 60% mixed-use rule] - evidence attached

(12 months of meter readings / charity reference number / floorplan

/ declaration). I am also submitting the attached signed VAT

declaration certificate to apply 5% going forward.

In line with HMRC's 4-year error correction window under VAT Notice

701/19, please refund the difference between 20% and 5% VAT for the

relevant period, totalling £[your calculated amount] across this

meter. Calculation breakdown attached.

Please acknowledge receipt within 5 working days and confirm a refund

decision within 28 days. If unresolved within 8 weeks I will treat

this as a formal complaint and escalate to the Energy Ombudsman.

Yours sincerely,

[Your name]

[Business name] | [Phone] | [Email]Customise the bracketed fields and attach: (1) signed VAT declaration certificate, (2) 12 months of meter readings or qualifying-status evidence, (3) your calculation spreadsheet showing overpayment per billing period.

Step 4: Track and Chase

Supplier processing timelines vary, but British Gas publishes a 28-day review target on its VAT reduction page (opens in new tab) - a reasonable benchmark to hold any supplier to:

- After 5 working days with no acknowledgement: send a chaser referencing the original submission date.

- After 28 days with no decision: send a formal complaint, marked as such.

- After 56 days with no resolution: you are at the threshold for ombudsman escalation.

A pattern worth anticipating: a supplier may apply 5% going forward and treat the going-forward change as the full remedy. If your eligibility for the earlier period is also clear, the backdated correction is a separate ask. Accepting the going-forward change without raising the backdated piece in writing can weaken your position later, so put the backdated request in writing as soon as the going-forward change is confirmed.

Step 5: Escalate If Refused

You have three options if the supplier digs in. They are sequential, not parallel:

- Formal complaint - written, marked “formal complaint”, reference HMRC VAT Notice 701/19. Supplier has 8 weeks to resolve.

- Energy Ombudsman - free for the customer, binding on the supplier. The Ombudsman provides independent dispute resolution for non-domestic energy customers and can review the supplier’s handling of the reclaim. You have 12 months from deadlock to file.

- HMRC error correction - VAT-registered businesses can claim through their VAT return under VAT Notice 700/45 (opens in new tab). Form VAT652 (opens in new tab) is for larger errors above the reporting threshold. This route bypasses the supplier entirely.

Citizens Advice has a useful summary (opens in new tab) of the formal complaint and Ombudsman process for non-domestic energy disputes.

What Evidence Suppliers Will Demand (and What They Will Reject)

Most refusals come from one of three evidence gaps. Anticipate them.

| Will be accepted | Will be rejected |

|---|---|

| 12+ months of supplier-issued meter readings showing under-threshold usage | Customer-provided readings only, or a 3-month sample |

| HMRC charity reference number with a written declaration | ”We are a not-for-profit” without a charity number |

| Floorplan or commercial schedule with the residential percentage marked | ”Around 60-70%” without measurement |

| Bills referenced by date, MPAN/MPRN, and amount | A single round-number total with no working |

| Written request specifying the 4-year period and £ figure | A general “please refund overpaid VAT” |

Submit everything in one package. Sending the going-forward VAT declaration first and the backdated request later means the supplier processes them as two separate tickets - and the going-forward piece tends to clear quickly while the backdated piece sits with a different team. A single submission with the declaration, the evidence pack, the calculated overpayment, and an explicit ask for the 4-year refund forces both to be handled together.

VAT-Registered? The Cashflow Story Is Different

If your business is VAT-registered, you already reclaim input VAT on energy bills through your quarterly VAT return - regardless of whether you paid 5% or 20%. The 5% rate does not change your long-term tax position.

Three things still make the reclaim worth doing:

- Cashflow. Reduced upfront VAT means smaller VAT outlay each quarter. For a business stretching cashflow, that is meaningful.

- Flat Rate Scheme. If you are on the FRS, your input VAT recovery is restricted - meaning you do not get the full 20% back through returns. The 5% rate applied at source recovers what the FRS would otherwise leave on the table.

- The Climate Change Levy bonus. Businesses that qualify for 5% VAT on de minimis grounds usually also qualify for Climate Change Levy exemption. The current CCL rate (from 1 April 2026) is 0.801p/kWh on both electricity and gas - the two were aligned for the first time at the 2026 update (see HMRC’s CCL rates guidance (opens in new tab)). CCL is a separate environmental tax, not VAT - it is not recoverable through your VAT return. So a single qualification check can unlock two separate cost reductions: VAT (claimable from the supplier) and CCL exemption (a permanent reduction going forward).

If you are not VAT-registered (under the £90,000 turnover threshold or voluntarily de-registered), the reclaim is pure cash recovery - the 15% does not flow back through any other route.

Possible Pushback Reasons (and How to Respond)

If a backdated reclaim is declined or partially declined, here are five responses you may encounter and a brief reply for each. These are based on the HMRC framework rather than first-hand customer experience.

1. “We can only refund from the date we received your VAT declaration.” HMRC treats an over-application of the standard rate as an overpayment of VAT, not a discretionary credit. Where eligibility for the earlier period is documented, the supplier can correct under HMRC’s 4-year error-correction window. Reference VAT Notice 701/19 (opens in new tab) and ask for the basis on which the backdated period is being declined.

2. “Your evidence is insufficient.” Ask exactly what is missing. A specific list of additional evidence is much easier to act on than a general refusal - and reasonable requests for proof are normal in this process.

3. “You were on a [contract type] that does not allow refunds.” Contract terms cannot override HMRC’s 4-year VAT error correction rule. The reclaim is statutory, not contractual - ask the supplier to confirm in writing how a contract clause overrides HMRC’s framework.

4. “We need approval from HMRC first.” The reclaim sits within the supplier’s own VAT error correction process. HMRC becomes involved only if the supplier itself files a separate error correction for amounts above the HMRC reporting threshold - which is the supplier’s process, not something the customer needs to wait on.

5. “We will refund forward but cannot process backdated.” The going-forward change and the backdated correction are separate but both available under HMRC’s framework. Ask in writing for the specific reason the backdated piece is being declined, and reference the 4-year error-correction window. Suggested reply: “I accept the going-forward correction. I am also formally requesting the backdated refund of £X for the period [date] to [date]. Please confirm the basis for declining this, or escalate to a formal complaint if it cannot be processed.”

What This Looks Like in Practice

A salon owner using around 9,500 kWh of electricity a year - well under the 12,000 kWh annual de minimis - charged 20% on a £3,800 net bill since 2022:

- Annual overpayment: £570

- Four years backdated (2022-2026): £2,280

- Plus CCL exemption going forward at 0.801p/kWh: ~£76/year

- One-off cost to claim: a few hours pulling readings and writing the request

Compare that to the time invested in switching supplier to save £400/year. The reclaim usually pays better per hour spent.

If the same salon is unsure whether they are on a deemed contract or a fixed deal, start by reading your bill correctly - the unit rate and standing charge lines tell you what type of contract you are on, which feeds into your evidence pack.

Suppliers Publish Their Own Backdating Policies

The 4-year reclaim framework is not just HMRC guidance - the larger UK energy suppliers publish their own customer-facing policies that align with it. Examples:

- British Gas: online VAT reduction application via the business portal, with a stated 28-day review target and the same de minimis thresholds (33 kWh/day electricity, 4,397 kWh/month gas). See the British Gas business VAT reduction page (opens in new tab).

- EDF: the EDF business VAT FAQs (opens in new tab) state “HMRC guidance allows EDF to backdate the relief for a maximum of 4 years (if appropriate)” and confirm VAT certificates can be backdated even if one has previously been submitted. The 60% mixed-use rule is also explicitly cited.

- E.ON Next: VAT declaration request via the business team (

hellobusiness@eonnext.com). E.ON Next’s published position is that businesses charged the standard rate when eligible for the reduced rate can apply for a partial refund backdated up to 4 years. - Other suppliers (Engie, SSE, Crown Gas & Power, npower Business Solutions and others) publish their own VAT declaration forms with backdating provisions, usually on the business or commercial-customer section of their website.

The consistency across suppliers exists because the framework is HMRC-driven, not supplier-discretionary. If your supplier’s VAT declaration form or backdating policy is not obviously published, ask their business team directly and reference HMRC’s VAT Notice 701/19.