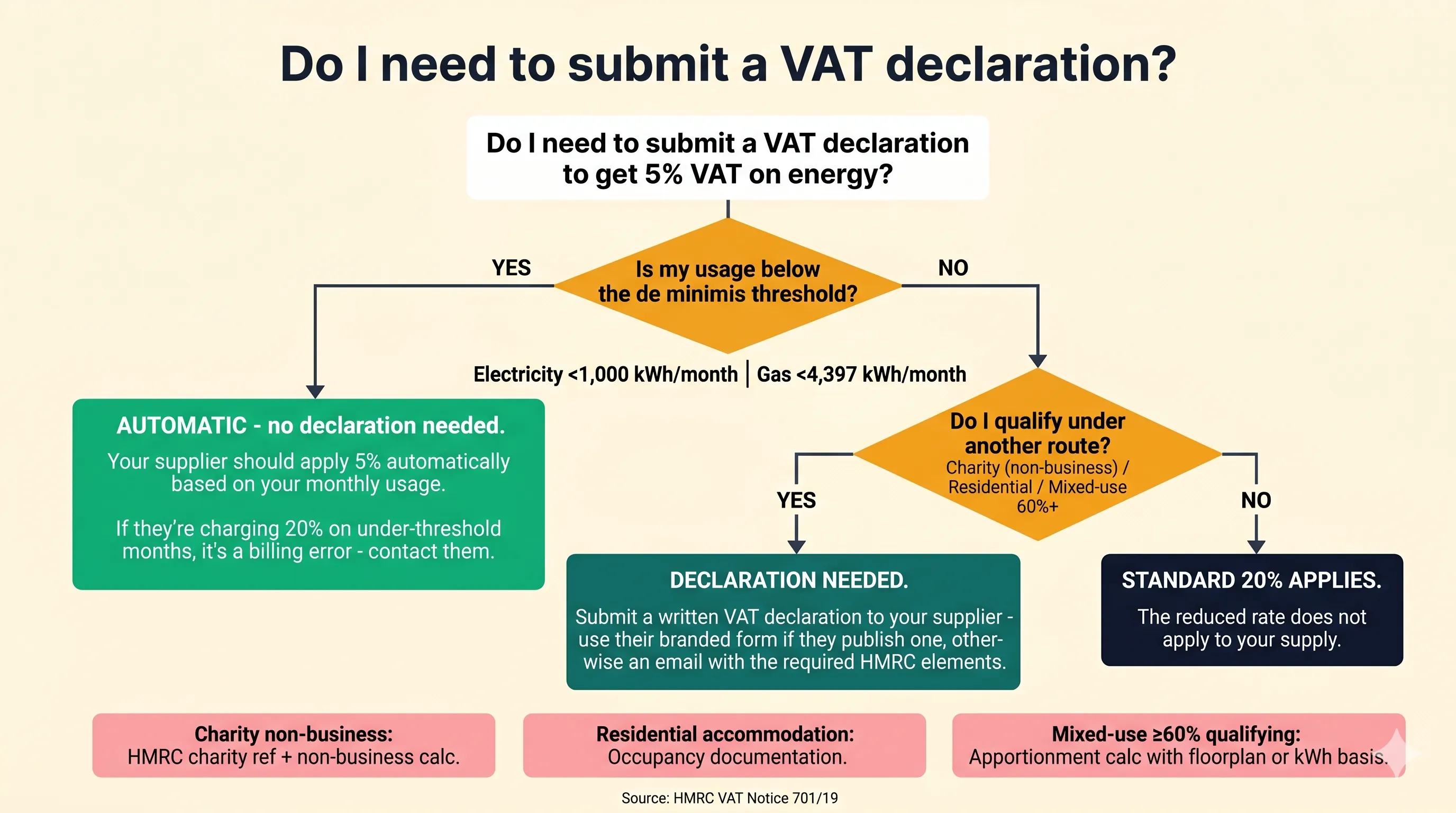

Quick answer: If your business qualifies for the 5% VAT rate on energy but the supplier is charging 20%, you need to contact your existing supplier and submit a written VAT declaration with supporting evidence. One critical exception: if you qualify under de minimis (below 1,000 kWh/month electricity or 4,397 kWh/month gas), the 5% rate is automatic - the supplier should apply it without any declaration from you. For every other qualifying route - charity, residential, mixed-use 60% - you need to submit a written declaration with supporting evidence.

This article walks through the process, the evidence each qualifying route needs, and how to verify the rate is actually applied. Most major UK suppliers have their own branded declaration form which is the fastest route; if your supplier does not publish a form, email their business team and they will either send you theirs or accept a written declaration containing the HMRC-required elements.

TL;DR

- De minimis qualifies are automatic. No form needed - your supplier should auto-apply 5% based on monthly usage. If they’re not, that’s a billing error, not a declaration issue.

- All other qualifying routes need a written declaration: charity (non-business activities), residential or quasi-residential premises, and mixed-use under the 60% rule.

- Contact your existing supplier first. Most major UK suppliers have their own branded declaration form - it is the fastest processing route because their billing system is designed around it. If your supplier does not publish a form, email their business team requesting the VAT declaration process - they will either send you theirs or accept a written declaration with the HMRC-required elements.

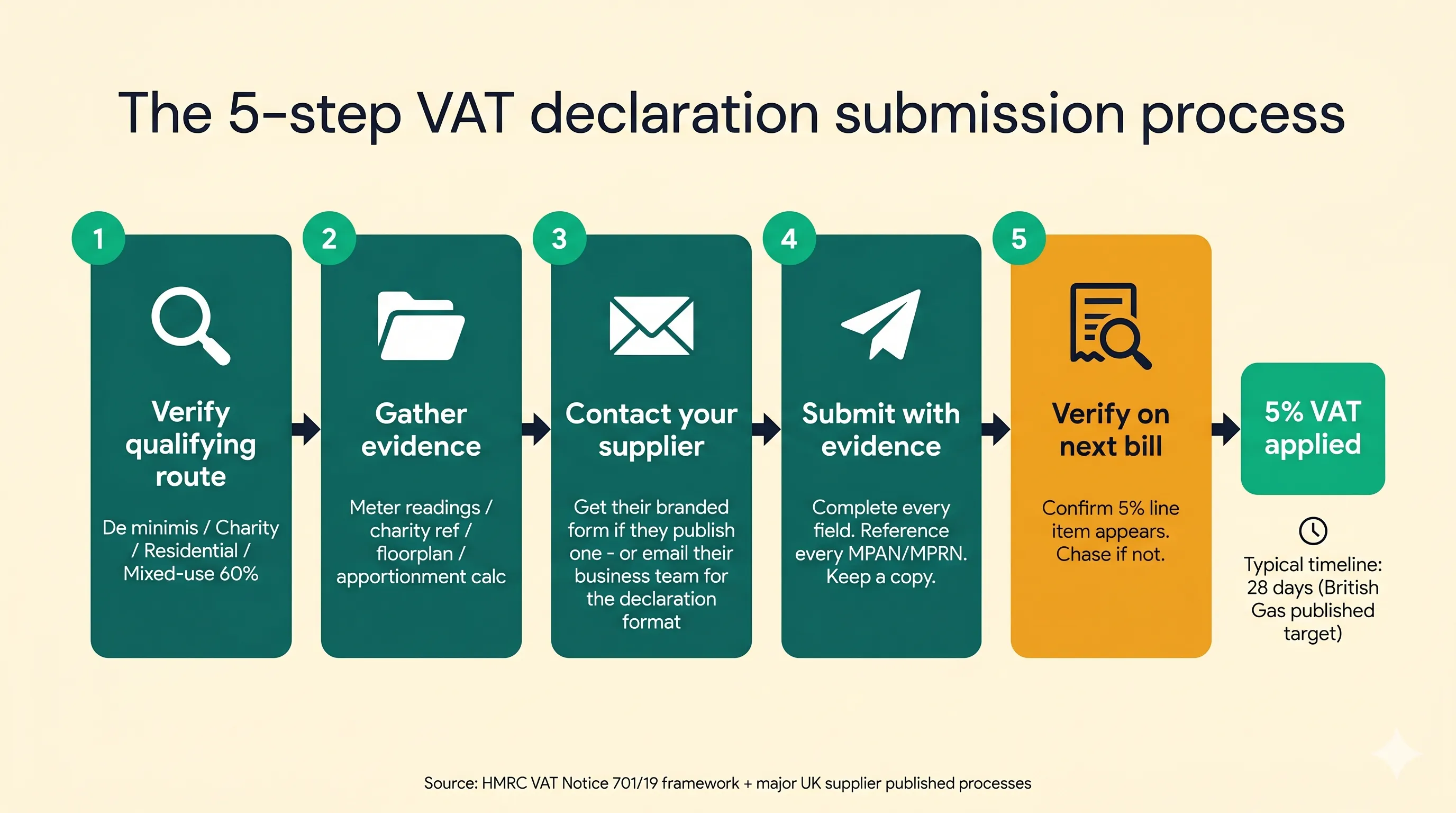

- Processing target is typically 28 days - British Gas publishes that explicitly; most other suppliers operate in the same range.

- Verify on the next bill - if 5% doesn’t appear after submission, chase with the submission reference.

- Don’t submit a declaration you can’t substantiate - if HMRC later finds it was inaccurate, the 15% VAT shortfall plus 7.75% interest (per HMRC’s late-payment rates (opens in new tab)) plus penalties up to 30% lands on the customer.

For the eligibility rules in full, see the master guide: VAT on Business Energy: 5% vs 20% Rules Explained. If you’ve already been overcharged at 20% when you should have been on 5%, see how to reclaim overpaid VAT.

When You DON’T Need to Submit a Declaration

The simplest qualifying route is de minimis: HMRC treats below-threshold business energy consumption as domestic-equivalent under VAT Notice 701/19 (opens in new tab). The thresholds are:

| Fuel | Daily | Monthly | Annual |

|---|---|---|---|

| Electricity | 33 kWh | 1,000 kWh | 12,000 kWh |

| Gas | 145 kWh | 4,397 kWh | 52,764 kWh |

If your consumption falls below the relevant threshold, the supplier should apply 5% VAT automatically - no declaration needed. The threshold is calculated per billing period, so a single high-consumption month (e.g. winter heating spike) flips that month to 20% even if your annual average is below the limit. Suppliers track this and bill accordingly.

Common scenarios where de minimis applies:

- Small high-street shops, cafés, salons

- Home offices and micro-businesses

- Seasonal businesses outside their peak months

- Empty or low-occupancy commercial units

If you’re under the threshold but being billed 20%, that is a supplier billing error rather than a declaration issue. Contact your supplier with 12 months of meter readings and request automatic application of the reduced rate plus any backdated correction.

When You DO Need to Submit a Declaration

Above de minimis, the 5% rate is never automatic. You submit a written declaration certifying your qualifying use. Three main routes:

1. Charity (Non-Business Activities)

For premises used wholly or partly for charitable non-business purposes - fundraising, worship, community services. You need:

- HMRC charity registration reference number

- A declaration that the energy is used for qualifying non-business activities

- If the premises has any business activity (e.g. a charity shop), an apportionment calculation showing the non-business percentage

Important: the “non-business” qualifier matters. A charity shop’s trading floor counts as business activity and that portion does not qualify. Worship space, free community programmes, and fundraising space do qualify.

2. Residential or Quasi-Residential Premises

Care homes, holiday lets, student halls of residence, places of worship, hospices. These qualify because the energy is used as domestic-equivalent supply. A single declaration confirms 100% qualifying use.

3. Mixed-Use (the 60% Rule)

If 60% or more of the energy at a premises is used for qualifying purposes (residential or charitable non-business), the entire supply qualifies for 5%.

Below 60%, you apportion - some at 5%, some at 20%. The apportionment calculation needs to be exact (not estimated) and use a defensible method:

- Floor area apportionment: qualifying square metres ÷ total square metres

- kWh apportionment: estimated qualifying kWh ÷ total kWh, with method shown

Suppliers want to see the calculation method, the input data, and the resulting percentage. Floorplans, occupancy schedules, or meter sub-readings usually accompany the declaration.

The 5-Step Submission Process

Step 1: Verify Your Qualifying Route

Be honest about which category you fit. If you’re at the borderline (e.g. close to de minimis monthly threshold, or under 60% mixed-use), the maths needs to be precise - this is the area where rejections concentrate.

Step 2: Gather Supporting Evidence

| Qualifying route | Evidence needed |

|---|---|

| De minimis | No declaration needed - but if your supplier is wrongly charging 20%, prepare 12 months of meter readings showing below-threshold usage |

| Charity (non-business) | HMRC charity reference number + declaration of non-business use + apportionment for any mixed activity |

| Residential / quasi-residential | Documentation of the use type (lease, licensing, occupancy schedule) |

| Mixed-use ≥60% | Floorplan or kWh schedule showing the qualifying percentage with calculation method |

| Mixed-use under 60% (apportioned) | Same as above plus the apportionment percentage that will be applied |

Step 3: Contact Your Supplier and Get Their Declaration Format

Most major UK suppliers publish their own branded VAT declaration form and prefer it because their billing system is built around it. Use that form if it exists - it’s the fastest processing route.

If your supplier does not publish a form (some smaller or newer suppliers do not), email their business team and ask for their VAT declaration process. They will either send you their form, point you at it, or accept a written declaration directly. Either way is acceptable under HMRC’s framework - what matters is that the declaration contains the required elements (qualifying basis, MPAN/MPRN, signature, effective date). The “Sample Submission Email” template later in this article covers the written-declaration route.

The next section lists the published forms and contact routes for nine major UK suppliers as a reference - if yours is on the list, start there.

Step 4: Submit the Completed Form with Evidence

- Customer name on the form must match the account holder exactly

- Reference every MPAN (electricity) and MPRN (gas) the declaration applies to

- Attach evidence pack as a single submission - splitting into multiple emails or uploads creates internal supplier ticket fragmentation

- Keep your own copy of everything submitted, with the date and any supplier reference number

Sample Submission Email (for email-based suppliers)

For suppliers that accept the declaration by email (E.ON Next, TotalEnergies, npower Business, Crown Gas, EDF on the PDF route), the form usually needs a short cover email alongside it. Copy and adapt:

Subject: VAT declaration submission - Account [your account number],

MPAN [your MPAN]

Dear [Supplier Business Team],

Please find attached our signed VAT declaration certificate for the

above account, certifying that our energy supply qualifies for the

reduced 5% VAT rate under [de minimis / charity non-business use /

residential or quasi-residential / mixed-use 60% rule]. We would

like the reduced rate to apply from [effective date].

Supporting evidence attached:

- Signed VAT declaration certificate ([supplier's branded form])

- [12 months of meter readings showing under-threshold usage /

HMRC charity reference [XXXXXX] / occupancy documentation /

floorplan with apportionment calculation showing [X]% qualifying use]

- [Any additional supporting documents]

The basis for our qualifying status is set out in HMRC VAT Notice

701/19. Please confirm receipt and the date from which the 5% rate

will be applied. We will check the next billing cycle to verify the

correct rate appears.

[Optional - include if you were eligible for earlier periods and

want backdated correction:]

I am also requesting a backdated refund of overpaid VAT for the

period [start date, max 4 years back] to [today's date], totalling

£[calculated amount] across this meter. Calculation breakdown

attached. This sits within HMRC's 4-year error-correction window.

Yours sincerely,

[Your name]

[Business name] | [Account holder name as on bill] | [Phone] | [Email]Customise the bracketed fields and attach: (1) the signed supplier-branded VAT declaration certificate, (2) supporting evidence matching your qualifying route (see the evidence table in Step 2), (3) for mixed-use submissions: the apportionment calculation showing your method and figures.

Suppliers using online portals or forms instead of email (British Gas, Engie, SSE Energy Solutions) replace this cover email with their portal’s submission fields - the same information goes in, just through a different channel. For backdated reclaim specifically, see our reclaim overpaid VAT guide for the fuller process and escalation path.

Step 5: Verify the Rate Is Applied on Your Next Bill

Check the next billing cycle:

- Look for a “VAT 5%” line item on the qualifying kWh

- Calculate manually: net energy charge × 5% should equal the VAT total

- If the bill still shows 20%, contact your supplier with the submission reference and ask why

- Confirm any backdated credit owed from the declaration’s effective date

Examples: How Nine Major UK Suppliers Handle VAT Declarations

This is a reference table for customers of these specific suppliers - it is not the definitive list of UK business energy suppliers, and a supplier not appearing here does not mean their process is any different in substance. The framework is HMRC-driven and consistent. The differences are operational - where the form lives, who you email, what the supplier prefers. Verified live as of May 2026:

| Supplier | Form / submission route | Notes |

|---|---|---|

| British Gas Business | Online VAT reduction application (opens in new tab) via the business portal | Published 28-day review target. Separate forms required for gas and electricity. |

| EDF | SME VAT FAQs page (opens in new tab) - branded PDF Customer Declaration Certificate | Can be backdated up to 4 years (HMRC framework) per EDF’s own published policy. |

| E.ON Next | Request form from hellobusiness@eonnext.com (business help hub (opens in new tab)) | Charity status accepted alongside de minimis. |

| TotalEnergies Gas & Power | VAT eligibility page (opens in new tab) - email to newstarts.uk@totalenergies.com (small business) or largebusiness.uk@totalenergies.com (large business) | Per their published policy, “without a signed declaration in place we cannot implement the reduced VAT rating.” |

| SSE Energy Solutions | ES-VAT Declaration Form V2 (opens in new tab) (January 2025 PDF) | Form requires exact MPAN and apportionment calculation. |

| Engie | VAT Declaration Certification page (opens in new tab) | Online certificate process. |

| Sefe Energy (formerly Gazprom Energy) | VAT help page (opens in new tab) | Per their published process. |

| Crown Gas & Power | VAT declaration page (opens in new tab) | Standard HMRC-style form via account team. |

| npower Business Solutions | Separate PDFs: Electricity (opens in new tab) and Gas (opens in new tab) - email to yourbusiness@npower.com | Spreadsheet template available for businesses with 10+ MPANs (request via the business team). |

If your supplier is not on this list, the same pattern applies - look for a “VAT declaration” or “VAT reduction” page in their business or commercial-customer section, or email their business team directly. If they do not publish a form, ask them to either send you theirs or confirm they will accept a written declaration. The regulatory framework is HMRC-driven and consistent across all suppliers, so the substance of what you need to provide does not change - only the format.

Common Rejection Reasons (and How to Avoid Them)

A few specific gaps account for most declaration rejections. Anticipating them keeps the process to one submission rather than two or three:

| Rejection reason | How to avoid |

|---|---|

| Customer name mismatch (form name ≠ account holder) | Use the exact account-holder name from your most recent bill, including any “Ltd” or trading-name suffix |

| Missing or wrong MPAN / MPRN | Pull these from a recent bill (13 digits for MPAN, 6-10 for MPRN) and include every meter the declaration covers |

| Estimated apportionment percentages | Calculate explicitly - floor area or kWh - and show the method on the submission. Suppliers reject “approximately 60%” or “we think 70%” without working |

| Incomplete fields | Treat every field as required even if it looks optional. Common omissions: effective date, qualifying period start, signature block |

| Generic HMRC form instead of supplier-branded | Always use the supplier’s own form |

| Out-of-date form | If the form is more than 12 months old in your downloads, check the supplier’s current version - SSE issued a new V2 in January 2025, for example |

| No supporting evidence pack | The form alone is usually insufficient for charity, residential, or mixed-use. Attach the documents listed in the evidence table above |

If a rejection is unclear, ask the supplier to specify exactly what’s missing. A specific list is much easier to resolve than a general “incomplete” response.

How to Verify the Rate Is Actually Applied

After submission, the rate should appear from the effective date you specified (often the next billing cycle, sometimes earlier).

The check is simple:

- Open your next bill

- Find the VAT line - it should read “VAT 5%” or “VAT at 5%” on the qualifying consumption

- Confirm the maths: net energy charge × 5% should equal the VAT amount

- If the bill is on apportioned VAT (e.g. 5% on 60% and 20% on 40%), the VAT line may split into two entries

If the rate is wrong on the bill:

- Contact your supplier with the submission date and any reference number

- Ask whether the declaration is accepted, in review, or rejected

- If accepted but not applied, this is a billing error - request a re-bill plus any rebate

- If rejected, ask for the specific reason and resubmit

For backdated rebates (where you ask for the declaration’s effective date to be earlier than the submission date): suppliers process these as separate credits. The going-forward correction usually appears within one billing cycle; the backdated rebate often comes through 4-6 weeks later. If you wanted backdated correction and only see going-forward, the backdated piece is still pending - don’t assume it’s been declined unless the supplier confirms in writing.

For a deeper walkthrough of backdated reclaim including escalation routes, see how to reclaim overpaid VAT on business energy.

Don’t Submit a Declaration You Can’t Substantiate

The risk on a VAT declaration sits with the customer who submits it, not the supplier who applies the rate. If HMRC later determines a declaration was inaccurate - either through an audit of your business or an audit of the supplier - the consequences are:

- Backdated VAT shortfall payable: the 15% difference between 5% and 20% for the full period the wrong rate was applied

- Interest at HMRC’s published late-payment rate (opens in new tab) (currently 7.75% as of 9 January 2026 - it tracks the Bank of England base rate plus 4%)

- Penalties under HMRC’s inaccuracy framework: up to 30% for careless error, up to 70% for deliberate (not concealed), up to 100% for deliberate and concealed

The qualifying routes are clear and documented. If you genuinely fall under de minimis, are a registered charity, run a care home or holiday let, or operate a verifiable mixed-use premises, you have nothing to worry about - the evidence supports the declaration.

Where to be cautious:

- Borderline de minimis - if you’re routinely close to 1,000 kWh/month, a single busy month is enough to invalidate that month’s 5% qualification. This isn’t a customer-side risk (suppliers track this), but it’s worth understanding before you expect 5% on every bill.

- Self-described “charity” without HMRC registration - “non-profit” is not the same as “charity for VAT purposes”. You need an HMRC charity reference.

- Mixed-use estimates that round generously upward - if the real qualifying percentage is 52% and the declaration claims 65% to clear the 60% threshold, that’s the kind of error HMRC sees as careless at best.

If you’re uncertain, take HMRC guidance via VAT Notice 701/19 (opens in new tab) or a tax adviser’s view before submitting.

What Happens After the Declaration Is in Place

The 5% rate continues to apply for as long as your qualifying status is unchanged. You don’t need to resubmit annually unless:

- Your usage pattern changes (e.g. you grow above de minimis on a sustained basis)

- Your apportionment percentage changes (e.g. you convert business floor space to charitable use)

- You change supplier (the new supplier needs a new declaration - they don’t inherit the old one)

- The supplier specifically requests confirmation

If your qualifying percentage changes, update the declaration proactively - suppliers won’t usually catch the change automatically, and continuing to claim a higher percentage than you’re entitled to creates the same backdated-shortfall risk as submitting a false declaration in the first place.

When you switch supplier, the old supplier’s declaration ends and you start the process again with the new one. Build this into any switch planning - if you’re on 5% with British Gas and move to EDF without submitting a new EDF declaration, EDF will apply 20% by default until the form is processed.